Form of separation: Functional

Infrastructure: TIM wholesale

Retail: TIM retail

Equivalence of access obbligation: EoI and EoO

Supervisory committee: Yes

Italy's Functional separation

- Functional separation*: Telecom Italia has a wholesale division department to provide access services both to TIM’s retail arm and also to alternative network operators (ANOs).

- Provisioning & assurance: TIM offers ANOs the possibility to choose a third-party company for provisioning and assurance of LLU and SLU services

- Supervisory board: Organo di Vigilanza (OdV) monitoring TIM’s compliance with undertakings and investigating any breach in non-discrimination obligations

- Unified technical delivery system: Both TIM Retail and ANOs use the same processes, the same systems, and the same databases

- Elements of equivalence: EoI: LLU, SLU, VULA FTTH services / EoO: VULA FTTC, WLR, BSA

- Netmap: The new network topology database implemented by TIM which gives the same information to TIM Retail and ANOs for the services activation.

*Project of voluntary legal separation notified to NRA in 20

Key facts

- Fixed broadband subscriptions by technology: xDSL – 86%, FTTH/B – 6%, FWA – 8%

- Incumbent’s retail broadband market share: Overall 43% – EU average 40% / xDSL 50% - EU average 53%

- Wholesale competitors: Open Fiber and Fastweb

- Major retail competitors: Vodafone, Fastweb, WindTre

Model of separation adopted

Italy currently uses a functional separation model. The Italian incumbent, Telecom Italia (TIM), has a wholesale division department to provide access services both to TIM's retail arm and also to alternative network operators.

TIM's wholesale division function has its own staff, information systems, investment budget, and a separate incentive scheme for wholesale staff and management. In addition, the Italian approach to separation includes a supervisory committee, Organo di Vigilanza (OdV), which is responsible for ensuring TIM's compliance with the principles of non-discrimination and equal treatment towards all ANOs accessing the incumbent's network.

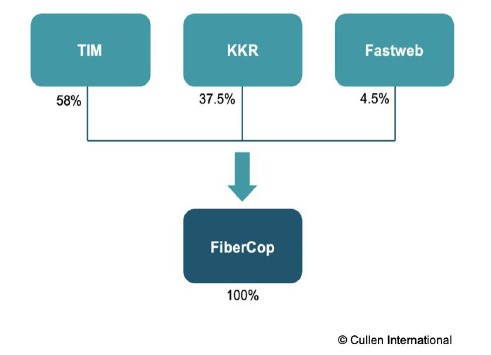

As part of a complex structure of transactions with an American investment company (KKR) and Fastweb, TIM notified a project of voluntary legal separation to the Italian telecoms regulator (AGCOM) for the creation of FiberCop.

Transaction structure (Cullen International)

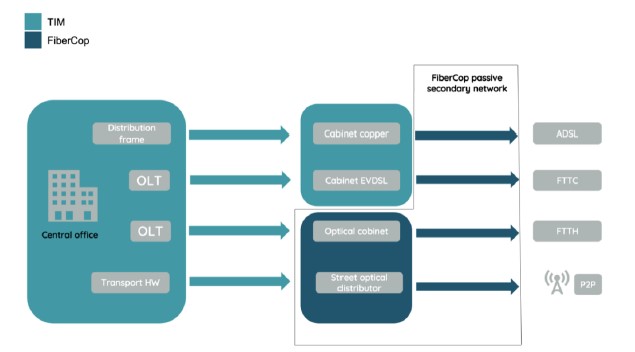

FiberCop (the NewCo) will include all of TIM’s passive secondary network infrastructure from the cabinet to the home both for fibre and copper, such as ducts and sockets (copper cabinets not included) along with the fibre network developed by FlashFiber, the joint venture in which TIM has an 80% and Fastweb a 20% stake.

FiberCop’s perimeter will not include street cabinets for copper (Cullen International)

TIM said that the NewCo will allow TIM, Fastweb and other operators to co-invest in fibre coverage across the country. TIM also signed a memorandum of understanding with another operator, Tiscali, to create a partnership to develop fibre broadband through Tiscali’s participation in the FiberCop co-investment plan.

AGCOM published a positive preliminary assessment of TIM’s voluntary separation project and opened a public consultation until 28 January 2021 with the aim to gather suggestions from interested operators. According to BEREC guidelines on separation and the Italian electronic communications code, AGCOM will go through a new fixed market analysis to assess the impact of TIM’s legal separation project on the existing regulatory obligations.

Furthermore, TIM and Cassa Depositi e Prestiti (Cdp, 82.8% state-owned financial institution pursuing a public interest mission) signed a letter of intent (LoI) to enable the creation of a single national fibre network (AccessCo).

AccessCo might be established through a potential future merger between FiberCop (in which TIM will contribute also its primary network) and Open Fiber (OF), a wholesale only operator rolling out FTTH 50% owned by CdP.

Organisational and governance structure

The organisational and governance structure of TIM’s model of separation has developed through a series of different regulatory steps and undertakings, summarised in the table below:

|

Step |

Date |

AGCOM decision |

Actions |

|

1 |

15 May 2002 |

152/02/CONS “Measures to guarantee internal and external equal treatment” |

|

|

2 |

11 Dec. 2008 |

718/08/CONS “Approval of TIM’s undertakings” |

AGCOM approved TIM’s voluntarily proposed undertakings, including:

|

|

3 |

5 Nov. 2015 |

623/15/CONS “Fixed market review M3a and 3b/2014 (split into decisions 652/16/CONS and 321/17/CONS) |

|

|

4 |

18 July 2019 |

348/19/CONS “Fixed market review M3a and 3b/2014” |

|

The Italian supervisory committee started in November 2015 to monitor TIM’s compliance with the undertakings set out in decision 718/08/CONS, which entered into force in January 2009, and on the new model of equivalence (NME) offered by TIM.

The Italian supervisory committee (OdV) is composed of five members, each serving a term of five years. Three members are designated by AGCOM and two by TIM’s CEO, after consultation with AGCOM. The president of OdV is chosen from one of the committee members designated by AGCOM. The staff of the OdV’s office are employees of Telecom Italia designated to support the work of the OdV committee with a mandate of three years, renewable once for a maximum additional term of three years. Staff must sign a code of conduct to avoid any potential conflict of interest with TIM including for confidentiality, independence and diligence. OdV has an independent annual budget of not less than €880,000.

In addition to overseeing TIM’s compliance with undertakings, OdV has started new forms of cooperation with AGCOM set out in annual workplans, such as:

- the development of a proposal for a new set of KPIs and KPOs linked to the NME (OdV’s proposal was largely reflected in AGCOM decision 395/18/CONS on KPIs);

- the proposal for a simplification and rationalisation of the causes of failed provision orders; and

- a study on the digitalisation of processes for monitoring delivery performance in work orders.

In the last fixed market review (AGCOM decision 348/19/CONS), AGCOM explained the new role that OdV will play until 2022, assuming that legal separation will take place. According to that decision, OdV will support the regulatory start-up phase of NetCo, offer technical support to AGCOM to monitor compliance with NetCo’s non-discrimination obligations, and gather input from the new regulatory compliance officers of Netco.

Whether OdV might play a similar role in the recent FiberCop voluntary legal separation project notified to AGCOM should be seen.

In addition, OdV will continue to monitor non-discrimination obligations, such as the new EoI model and the new KPIs set out in in decision 395/18/CONS.

Elements of equivalence and non-discrimination

On 5 November 2015, TIM's board approved a "plan to introduce a New Model of Equivalence, aimed at further strengthening the efficiency and effectiveness of the delivery and assurance processes" for its wholesale access services.

The aim of the NME is to ensure that the sales divisions of TIM have an equal footing with those of the ANOs for more effective internal and external equality of treatment and for greater transparency in the management of line activation requests.

Currently, TIM must assure EoI (also called the full equivalence model) to ANOs for LLU, SLU and VULA FTTH services, whereas it must assure only EoO (described as an enhanced EoO "equivalence +") for VULA FTTC, bitstream and WLR shared access services.

As part of the new equivalence model, TIM also implemented:

- unified technical delivery system (Nuova Catena di Delivery) for both TIM Retail and ANOs to use the same processes, systems and databases for analysis of technical coverage and topology, order validation and acceptance, formal and commercial checks, assessment of technical feasibility, and order management and creation of the intervention request; and

- new network topology database (Netmap) which gives the same information to TIM Retail and ANOs for service activation.

In addition, TIM implemented the disaggregation of provisioning and assurance for LLU, SLU and VULA FTTC. This means that TIM gives ANOs the possibility to choose a third-party company (Impresa System) for provisioning and assurance in relation to the abovementioned services. These third- party companies are selected by TIM based on criteria such as reliability, competence, and financial stability, established in accordance with AGCOM.